Mergers and acquisitions have similar reasons to those described in Chapter 5 when dealing with international alliances. A merger and acquisition case differs from an alliance because of the ownership structure. On the other hand, mergers and acquisitions are considered as equity alliance. In a non-equity alliance, the partner organizations remain independent of each other in terms of capital ownership. During mergers and acquisitions, the organizations get associated with mutual ownership.

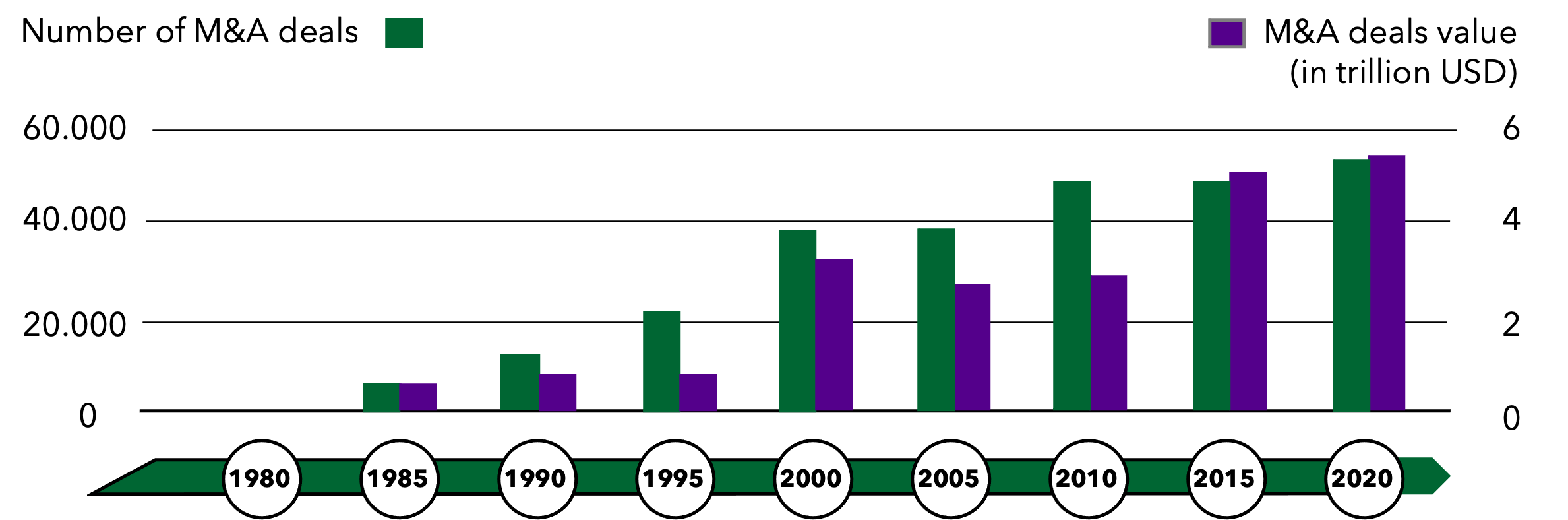

An international merger or acquisition is usually considered as a foreign direct investment if more than 10 percent of the shares with voting right of an organization operating abroad are purchased. The name “merger and acquisitions” is commonly used all over the world, but depending on the specific legal system of the country and the investment strategy of the companies, even a merger, when two identical organizations decide to merge, still involves an acquisition of shares. Thus, either one organization acquires the shares of the other, and then the acquired organization is liquidated by merging it with the parent company, or both organizations claim a new legal entity and transfer all or part of their resources to it. In the case of international foreign investments, an option is possible when two companies establish a joint venture in another country. The beginning of the merger and acquisition boom is in the 1990s (Exhibit 6-13). Moreover, at the same time, the number of strategic non-equity alliances and cooperation business networks involving international organizations has increased in the world. To expand in other countries, corporations had to either establish or acquire organizations operating there or enter into strategic non-equity alliances with companies operating in those countries. In the last decade of the 20th century, a real race started, the goal of which is to overtake competitors in competing for the advantages provided by globalization and the advantages of the global organization over the local company. The speed factor encouraged companies to acquire or merge with existing companies abroad, rather than creating greenfield investments from scratch. The need to overtake competitors and be the first to become the market dominating organization in a specific industry encouraged choosing a faster way.

Acquisitions and rapid expansion at the same time in many countries around the world required huge investments. Buying the shares of many organizations operating in various countries was a challenge even for organizations that were already international at that time, so mergers appeared to be an attractive alternative then. Shareholders of many multinational companies in various industries have decided that it is better to have partial control of a global organization than full control of a local one.

Ex. 6‑13 Mergers and acquisitions growth

Keywords: M&A, foreign investment

Source: Adopted from World Bank Group, www.worldbank.org

Mergers have occurred in various industries like automotive industry, the computer industry, the pharmaceutical and chemical industries. Entrepreneurs, seeing the benefits of becoming a global organization, agreed to give up control of their own business and share control of an already global business with the shareholders of an international organization. Many mergers took place in the US, Europe, Asia. There was a lot of mergers between US and European companies.

When acquiring an organization or merging with another company, there are many complex questions that arise, the most important of which is the price paid for the shares, or the value of the organizations if they merge, as this will determine the proportions of the shares of the overall company. Thus, at the end of the 20t century, the services and methods of determining the value of international companies became extremely important. In the case of most acquisitions and mergers, such methods as book value, real value of assets, market price and profit indexation are used (Exhibit 6-14). Book value is one of the rarest methods because it reflects the nominal value of the company’s shares and the value of the equity capital as it is recorded in the company’s accounting documents, that is, the balance sheet. This value is also called the company’s “Balance sheet” value. Often, the balance sheet values did not reflect the true value of the company. For example, an asset included in the balance sheet may be formally considered depreciated, but it is still functioning, and such an asset can be sold in the market at a significantly higher value than the balance sheet value. Thus, the assessment of the real value of the company’s tangible and intangible assets is a method that allows determining a more accurate value of the company’s assets, more specifically, individual asset units in the market. The market price of the business itself allows an investor to see the price that someone has actually paid for the shares of a similar organization in the market. This method may appear to be the most accurate at first glance, but it has several application limitations. First, the purchase and sale transactions of similar organizations must be carried out in the market. Not necessarily such transactions have been completed, but in addition to what can be considered similar companies. Seemingly, similar companies can be very different in their technology, their customers, and therefore their values can be very different.

The acquisition value is not always disclosed but kept confidential. The fourth method is called profit indexing, which means that the value is equal to the average profit of its last few years of profit multiplied by a certain number of years. For example, if the company’s average profit was 50 million Euros, then its value after agreeing to be indexed 5 times would be 250 million Euros. In other words, the investor can expect to earn 250 million Euros over the next five years. If an investor knows what Return of Investment – ROI rate of investment satisfies him, he can easily calculate how many times he agrees to index the profit when determining the value of the company. In this example, if the investor pays 5 times the indexed earnings price for the company, that means the return on investment will be 20 percent. So, the investor has to decide whether such an attractive investment satisfies him. This method is based on the assumption that the organization will be just as profitable in the future as it has been in the past. Foreign investment is made with an intention to achieve higher profitability, and this can be achieved by leveraging the advantages arising from the international nature of the business.

Mergers and acquisitions – M&A is a type of international development is more of an instrument that is used both in strategic foreign investments and in vertical alliances and in horizontal alliances. In the case of a merger, two companies come together to form a new company, while in the case of an acquisition, one organization acquires the shares of the other. Both forms are often considered an alternative to greenfield investments when establishing and starting a business abroad.

Ex. 6‑14 Pricing methods in an acquisition

Keywords: price, shares acquisition, M&A

Advantages of international mergers and acquisitions:

- It is a good instrument to accelerate foreign direct investment and international development.

- The number of customers increases very quickly, especially in the case of a horizontal equity alliance.

- An international organization based on capital ties maintains control and management discipline.

- Each organization can take over knowledge, experience, abilities from a partner organization linked by capital ties.

- This method is much faster than greenfield investments abroad.

Disadvantages of international M&A:

- It is a more expensive method than a non-equity alliance in an alliance, as well as more expensive than a franchise or export.

- In the case of acquisitions and mergers, two different organizational cultures, traditions and employee habits have to be reconciled, which often causes resistance.

- If two equal companies of a similar size merge, competition between the management often arises, because the former manager and his team of one organization will have to give way to the manager and team of another company; the importance and potential impact of personal ambitions cannot be underestimated.

Share or comment this information on your social media:

Fundamentals of global business

First edition

For citation:

Jarzemskis A. (2025). Fundamentals of global business, Litibero publishing, 496 p.

Full scope of the book is available in various formats

B.6. Foreign investments

- International resource movements

- Foreign direct investments

- Foreign portfolio investments

- Pros and cons for investing abroad

- Incoming foreign investments

- Management and design of foreign investments

- Attraction of foreign investments and free economic zones

- Mergers and acquisitions

- Questions for chapter review

- Chapter bibliography

About author

The author has been teaching at several universities since 2005. 40+ scientific publications, 10+ international research projects. More about author.