Around the world, countries have different economic systems and different indicators. Essentially, four economic systems can be distinguished – market economy, planned economy, hybrid economy and transition to market economy. Economic systems are influenced by the structure of a country’s political system. Countries that possess strong left-wing political ideology continue to adhere to the doctrines of communism and organize their economy in a planned way. The best example of a planned economy was the planned economy of the Soviet Union during the 20th century, where private business initiative was not allowed, and all enterprises were owned by the state. Since there was no market available, the prices were determined in a planned manner. For example, when a product was made of metal or plastic, the price would simply be physically stamped into the product (Exhibit 8-11).

Salaries for employees were determined in a planned way, and jobs were simply assigned by force based on the level of education and field of profession. The Soviet Union was able to survive just due to the export of extracted raw materials. Natural resources such as oil, gas, ferrous and non-ferrous metals supported the country’s economy, before it collapsed in 1990 (Kornai, 1992). Although today the planned economy seems like a utopia and an incomprehensible phenomenon to a Westerner, its elements still exist. For example, China basically has a planned economy with a mix with benefits of a market economy. For many decades, significant companies are owned by the Chinese state, which has been ruled by one party, the Communist Party. Even private companies have relatively limited freedom to operate compared to the freedoms enjoyed by companies in North America, Europe or Australia. Some countries regained their political independence after the collapse of the Soviet Union, so they had to transform their economies from a planned to a market economy (Huntington, 1991).

Ex. 8‑11 Price stamped into the product

Keywords: regulated economy, fixed price

The main areas of the economy and indicators that are important for international business are the country’s gross domestic product, the country’s gross domestic product per capita, the demographic situation, the average salary in the country, the demand and supply of labor, the transport and communication infrastructure in the country, the tax system, banks and availability of financial markets, national currency and its exchange rate, inflation rate. Each of the economic indicators has a different significance when choosing the type of doing business in and with foreign country (Exhibit 8-12).

Source: author’s photo

Ex. 8‑12 Significance of economic indicators when considering the type of business internationalization

Keywords: economic indicators, business internationalization

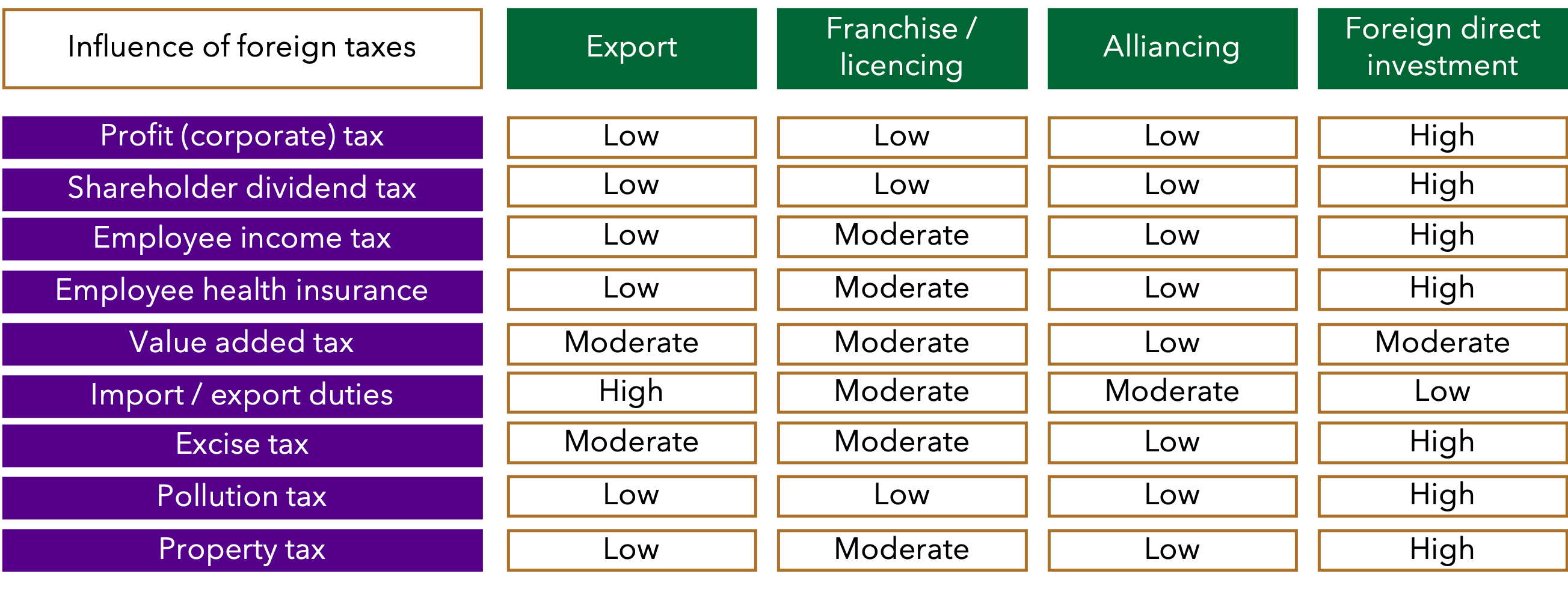

Some indicators are very important when it comes to market size and consumers purchasing power. This holds significance in the case of export, as well as partially in franchising and licensing. In certain cases, the customers market is also important when planning direct foreign investments or an alliance with a foreign company. The consumer’s market is best characterized by the number of inhabitants as it represents market size. The gross domestic product per capita and the average salary in the country, represent the purchasing power of the population.

The cost of labor, the availability of financing, and the supply of labor are important when planning investments in a foreign country, especially if production or assembly is planned there. Foreign exchange rates and their stability are usually important for all cases of international business, because a sudden decrease or increase in the exchange rate can cause unexpected consequences and distort the achievement of the financial forecasts of the business plan very strongly. Higher salaries in target country are a favorable factor for export there, but negative for foreign direct investment.

Gross domestic product is one of the most widely used indicators to assess the economic capacity and wealth of any country. The largest GDP calculated at current prices in US dollars in 2022 is calculated in the USA, followed by China, Japan, Germany, India, the United Kingdom, France, Russia, Canada, Italy, Brazil, Australia, Korea, Mexico, and Spain. The fact that China is catching up with the United States, India is ahead of the United Kingdom, Mexico is ahead of Spain, Brazil is ahead of Portugal shows the ongoing levelling of the world economy, where countries that were colonized a few centuries ago began to overtake their historical colonizers in the 21st century.

With Globalization, free business decisions to move production resources and the better conditions for this, the countries of Southeast Asia and South America begin to seriously compete with European countries. After Europe and USA achieved a higher standard of living, it began to raise labor and environmental standards and strive for quality of life, but at the same time, countries in Asia and South America, which do not raise such standards, are gradually taking over economic power.

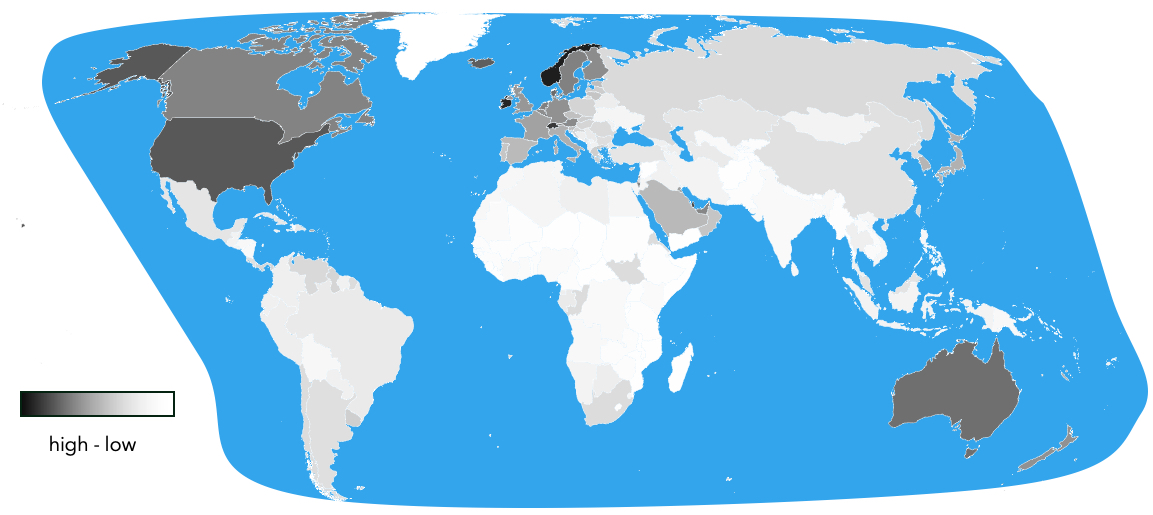

However, it is very important to evaluate another indicator – GDP per capita. According to this indicator, Monaco leads, followed by Luxembourg, Bermuda, Norway, Ireland, Cayman Islands, Switzerland, Qatar, Singapore, United States of America, Iceland, Denmark. Islands that have favorable tax systems and small populations, such as Bermuda or Cayman, become attractive locations for international companies to register, thus greatly increasing the GDP per capita of these countries. According to this indicator, China shares lowest positions in TOP50, and India is even below TOP 100. Still, China and India have a global population of about 1.4 billion each. So, a third of the world’s population is living in those just two countries. Average purchasing power in those Asian countries are small. Highly populated Asian countries are very attractive to investors who want cheap and abundant labor. At the same time, it is important to understand that the average GDP per capita does not reflect full picture of the consumer market. It would be mistaken to believe that China or India do not have a large enough market with high purchasing power. Despite the fact that one percent of the population in this country possess a high level of wealth or income, it is worth noting that out of the total population of 1.4 billion, 14 million individuals possess high level of wealth, which is comparable to the total population of the Netherlands. China is even becoming famous for its billionaires and is challenging the United States with this indicator.

Ex. 8‑13 Map of GDP per capita

Keywords: GDP, countries, inequality

Source: adopted from Statista, www.statista.com

Aggregate GDP is often more important than GDP per capita when assessing a country’s overall economic and political influence (Exhibit 8-13). Aggregate GDP shows a country’s ability to accumulate funds that are collected by the government in the form of taxes. Having a very large potential of accumulated funds, the states can afford to develop space, nano or bio technologies, advanced military technologies and civil infrastructures. Thus, the GDP and even a size of a state’s population remain an important economic and political lever and factor in international relations. For instance, there are seven countries in 2024 in the world that officially possess nuclear weapons: the United States, Russia, France, the United Kingdom, Israel, India and China, Pakistan and North Korea.

To compare the GDP per inhabitant in 2022 between Monaco (240 thousand US dollars), Norway (108 thousand US dollars), US (76 thousand US dollars) and Chinese currency is equivalent to 12 thousand US dollars or while Indian currency is equivalent to 2.4 thousand US dollars. The differences can be seen from several times to even 100 times. When evaluating the buyer’s market for exports, it is best to assess the GDP per capita, the total population and specific market segments, which may be exceptions or certain marginalities.

The largest GDP per capita are in European and North American countries, these indicators are also quite high in the United Arab Emirates, Israel, and Kuwait. Among countries of South America, Argentina has the highest rate, but it is only slightly higher than China. In Mexico, Brazil and number of other South American countries, this rate is lower than in China.

China’s total GDP and GDP per capita grew significantly as US and European companies invested impressive sums in manufacturing and assembly in China during the last decades of the 20th century and the first decades of the 21st century. China’s GDP per capita has more than doubled from 2010 to 2020. Due to China’s geopolitical ambitions and the challenge posed to the United States and the European Union, many international companies from these countries began to consider moving production resources to India or South American countries in the third decade of the 21st century. The countries such as India and some in South America, due to their GDP per capita and wages, become very competitive in attracting FDI compared to the economically strengthened Chinese society.

An important indicator for international business is the transportation, logistics and communications infrastructure. To serve international business, well-developed seaports with suitable and deep enough quays to accommodate the largest ships, large-volume container transshipment terminals in ports, railway lines and access and highways connecting factories to ports are very important. Among the world’s 10 largest ports, as many as 7 are in mainland China, one in Singapore, one in Hong Kong, and only 10th is a port in Europe – Rotterdam. Geography of largest container ports is reflected in chapter 13.

Thus, it is impossible to transfer large-scale production resources easily and fast from China to India or Mexico, for example, again due to technical and infrastructure limitations.

Ex. 8‑14 Taxes to consider for international business

Keywords: tax, duty, VAT, health insurance, social security

The construction of transport infrastructure, such as ports or railways, is estimated to require hundreds of billions or even trillions of dollars of investments. However, countries that collect a sufficiently large amount of GDP can afford it, and India in the 30s of the 21st century is just starting to make significant investments in transport infrastructure that could serve global business. Therefore, the third decade of the 21st century is becoming a period that significantly disrupts the established order and traditions of global business.

The tax environment is one of the most important parts of the economic business environment (Exhibit 8-14). General tax principles are maintained in many countries of the world and tax systems can be considered similar, but the biggest differences are revealed through the amount of specific taxes. The main forms of taxes that are relevant when conducting international business are:

- A corporate or profit tax for enterprises.

- A dividend income tax for shareholders.

- An income tax for employees.

- A health insurance tax for enterprises and employees.

- A value added tax for enterprises.

- A tariff on import and export.

- An excise taxes on products and services.

- A tax for pollution.

- A tax for property and real estate.

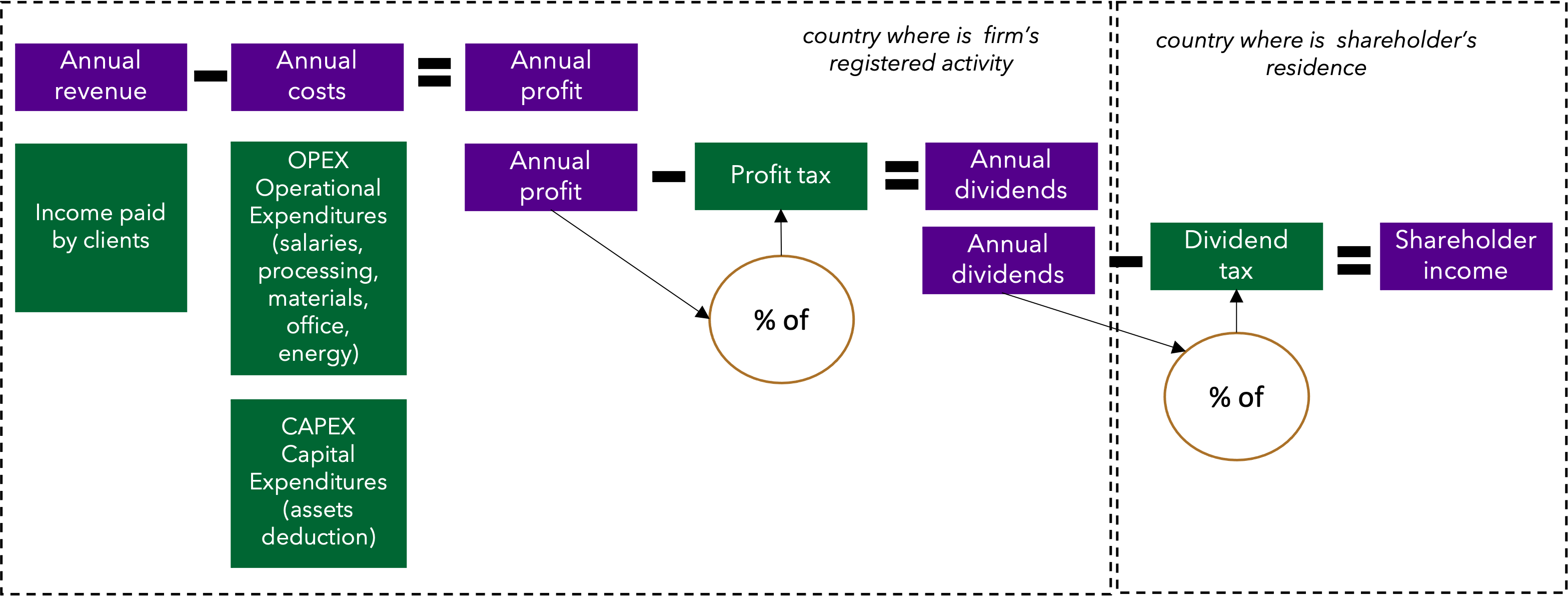

One of the most important tax forms is corporation tax. That is what it is called in the USA, and in some countries of the European Union. However, this tax is also called profit tax in many countries. The essence of this tax is that the organization must pay a tax to the state in which it operates, which is calculated as a percentage of the company’s profit (Exhibit 8-15). In some countries, tax is paid on the previous year’s profit, which is calculated and declared to the tax authority. In some countries, there is an obligation to pay the so-called early profit tax, which is paid in advance for the current year, based on the profit of the previous year. When the current year’s is closed and profit is finally calculated, there remains possible corrections of the profit tax that was paid in advance – part of it may be returned to the company, so depending on actual profit it could be necessary to pay missing gap additionally or return overpaid tax.

The profit tax is paid depending on the annual profit, which is calculated from the total income received by the organization after deducting the costs of the company, during the same period, for example during the calendar year. If the organization incurs costs more than it receives income, then the organization does not pay profit tax, and the incurred loss can be leveraged with the next year’s profit. Each country has different rules on purchases of goods or services made by an organization that can be included in the expenses register of the company. Costs that are defined by law as eligible are called profit-reducing costs. For example, an organization purchase of a luxury car may be treated as an improper expense in some countries, especially in Europe, so it may not reduce profits.

Although such inappropriate costs are also recorded in the company’s accounting documents, they are not deducted from the company’s income when calculating the profit. In states with more left-leaning political leanings, laws tend to restrict many of a company’s spending from being included as profit-deducting expenses, especially luxury goods. So, in fact, in such countries, the taxable profit for the organization is calculated higher than it really is. So, the profit tax calculated is also higher. The percentage of corporate or so-called profit tax varies from country to country. The most common is 15 percent tax rate, but there are countries that apply 20-25 percent. or even 35 percent, there are also countries applying 5 percent, profit tax, or even 0 percent. The corporate tax in the US is 21 percent, it varies in the countries of the European Union, but on average it is 21.3 percent. In some countries, this tax depends on the industry, in others it depends on the firm’s total revenue. For industries in which the country has an interest in encouraging investments, for example Algeria, applies a reduced tariff. Some countries apply a reduced profit tax rate for small companies, for example Australia, Lithuania. Some countries, for example India, apply an increased rate for taxing the profits of companies with foreign capital as 40 percent.

Ex. 8‑15 Taxes to consider for international business

Keywords: tax, duty, VAT, health insurance, social security

Profit tax is important for foreign investors. This tax makes India, Mexico, major South American countries still look less attractive than China. The desire of the government of these countries to collect more taxes is understandable, but as investors look for an alternative to China, the countries should see their corporate tax competitiveness well, even compared to the US or European countries. Eastern and Northern Europe look quite attractive for investments. For example, the profit tax in Bulgaria and Hungary is 9-10 percent, in Lithuania only 15 percent, in Poland – 19 percent, in Estonia, Latvia, and Finland – 20 percent each. Some countries require the payment of the tax only if the shareholders decide to pay dividends. If the profit remains in the company, for example, Poland does not require corporate tax payment. Tax incentives in free economic zones also apply. In China, a very large amount of investment in the first decade of the 21st century came precisely to the southern eastern coasts of China, which not only had good logistical access, but in many places operated free economic zones that provided tax relief.

Another important tax, which is related to the profit tax, is the taxation of the dividends received by the shareholder from the profit. Base to calculate dividends is the profit after profit tax paid. If the shareholder of the organization is another company, i.e. parent company, then the profit received from the subsidiary becomes the income of the parent company, which is accounted as income from financial – investment activities. The parent organization pays corporate tax depending on its country of operations at its own country’s rates. If the shareholder of the organization is a natural person, then he must pay the income tax of a natural person, which is calculated from the amount of dividends paid out, when he pays profit to himself. Personal income tax can be calculated either according to the tax rates of the country where the dividends were earned or according to the tax rates of the country where the person lives and is registered as resident. Some countries set tax rules and requirements to be paid specifically in their own country, but the general principle is to ensure that the same person is not taxed twice in their own country. Many countries have signed a wide variety of mutual agreements on the avoidance of double taxation, but the provisions of each agreement vary. Due to each case, it is necessary to examine the mutual agreement between the specific countries and the legislation regulating taxes.

The simplest example could be a situation where the corporate tax rate is 20 percent, and the income tax of the shareholder as a natural person is also 15 percent. In this case, if the profit is 1 million dollars, then the profit tax paid by the organization is 200,000 dollars. In this case, the remaining 800,000 is paid to the shareholder after taxing it with an additional 15 percent. at a rate of 120,000 dollars. The actual after-tax money going to the shareholder is 680,000 dollars. So, in example, the accumulated profit taxation for the investor or shareholder at 32 percent. When the shareholder of the subsidiary organization is the parent company, basically the same principle applies, the profit of the subsidiary organization is taxed first, and the profit received by the parent organization becomes income, which increases the profit of the parent company, so it is taxed again. To reduce the tax burden, some countries agree on tax exemptions, especially in cases where the profit is not actually paid to the shareholder but is left in the organization as asset. International accounting principles are quite complex because different countries have different tax laws, there exist diverse tax treaties between countries, and taxes are frequently reviewed and modified, so international companies often purchase professional services and tax consultants and auditors to help ensure compliance with the law. Due to the dynamic and varying nature of this field, international tax and audit consulting organizations with offices in many countries around the world provide services to multinational organizations.

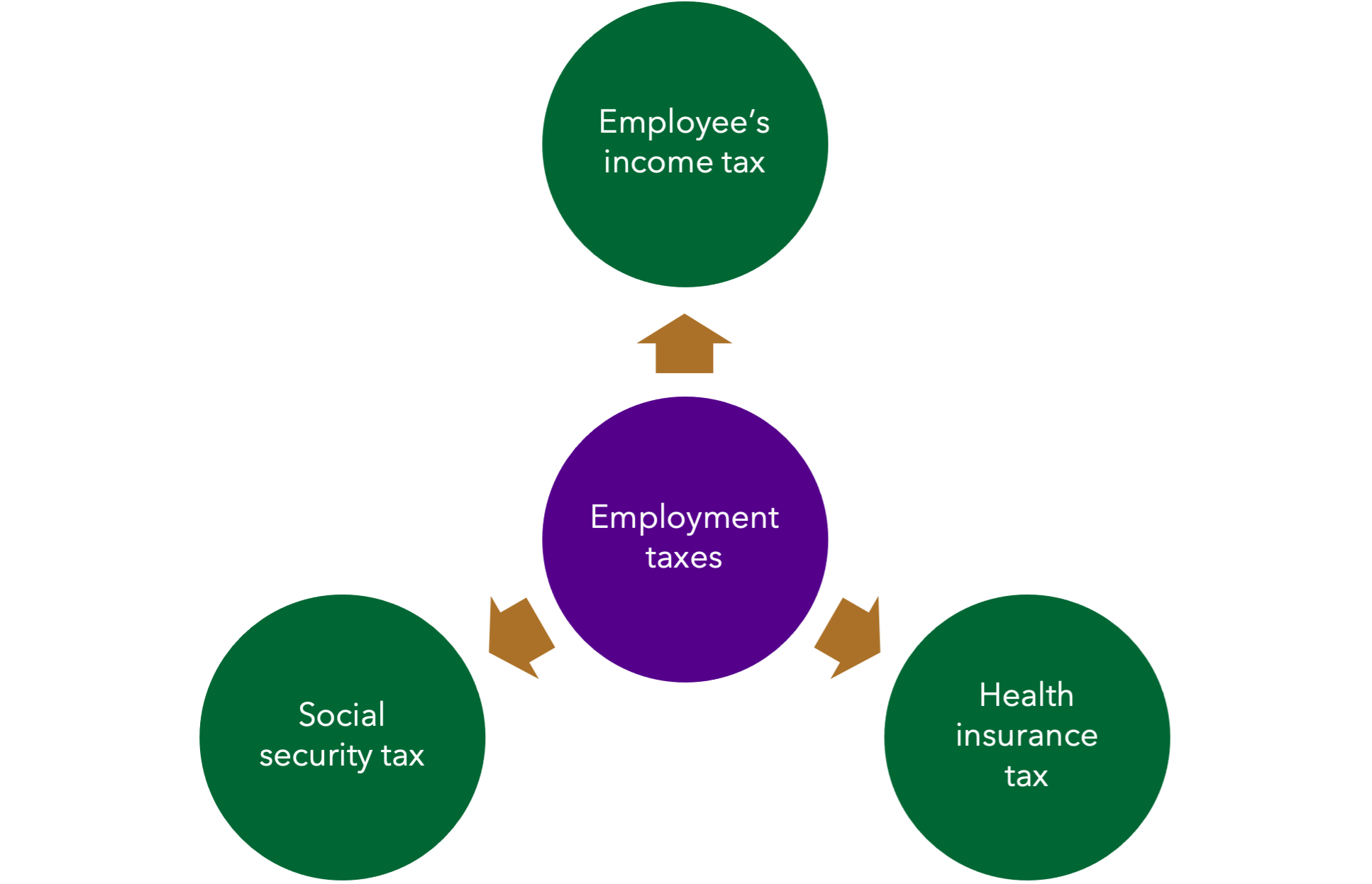

Employment-related taxes also vary from country to country, with tax types, structure and rates varying much more than corporate income tax (Exhibit 8-16). One of the most important differences is related to the taxpayer himself. For example, in the United States and some other countries, the obligation to pay taxes lies with the employee himself. In this case, the employer pays the employee the agreed salary at the agreed regularity – weekly or monthly, and the employee is liable to pay taxes to the state himself. Each employee has a different amount and percentage of taxes, because there is an opportunity to reduce the taxes paid by declaring certain purchases to the state. Thus, in countries with this type of tax system, each resident accumulates evidence of incurred expenses, and pays taxes once a year, every six months or every quarter, depending on the country. In such countries, workers are considered to be less protected by the state and the employer. The employee is not only responsible to pay the mandatory income tax to the state, but also to decide about his health insurance and pension accumulation. Basically, the US is the best example of this model of employees’ income, health insurance and pension system. This tax is a consequence of the prevailing long-term right-wing political direction. The complete opposites are countries with a very strong left-wing political direction and social policy. In such countries, it is the responsibility of the employer to pay taxes for the employee.

Ex. 8‑16 Taxes to consider for international business

Keywords: income, health insurance, social security

Thus, the organization transfers taxes for the employee to the state tax office. In some countries, these fees are included in the employment contract, and when signing the employment contract, the employee and the employer indicate the total amount of the salary including all taxes. However, there are countries where the employment contract specifies only a part of the taxes to be paid by the employer, such as resident income tax, but other taxes, such as social insurance, pension insurance, solidarity, health insurance, are not reflected in the contract, but as per the law it has to be paid by the employer. It is very important to know these differences, because when an organization is preparing to invest in another country, it can make mistakes in the business plan if it fails to consider that there will be taxes in addition to wages, are crucial components of labor cost. Every investor in another country must verify the specifics of that country’s taxes and correctly assess the full cost of labor, including all related taxes. Taxes such as social security or health insurance can often amount up to 30 or 40 percent of the total salary. In many countries of the European Union, these taxes are quite high, because a state fund health care or state pensions there. Thus, in some states, residents who work under employment contracts automatically receive the so-called free medical and health care and receive guaranteed state pensions. The higher the taxes, the more the state ensures greater social welfare and equality for its citizens. Knowing these differences is important not only for international business owners, but also for employees who work for international companies and are sent to other countries to work in organization divisions. For example, the amount of salary received in the USA may appear to be very high compared to Europe, but when considering that the employee pays all taxes by himself and also has to pay to private health insurance and to private pensions, the real actual income after all deductions may no longer be the same competitive as in Europe.

Ex. 8‑17 Taxes to consider for international business

Keywords: VAT, deduction

Employee Income Taxes in various countries of the world range from 10 percent, for example in Kyrgyzstan, to 50 percent, for example in Slovenia or the Netherlands. The US tax is 37 percent, but it has various deductions. Some countries have a so-called progressive tax system, the higher a person’s salary, the higher the percentage of taxes calculated. For example, in the United Kingdom, if a person earns more than 125,000 pounds per year, the tax is 45 percent. If the income tax paid by the employee is added together with the social insurance or solidarity or health insurance tax, the average amount of taxes in various countries of the world begins to variate between 40 and 60 percent.

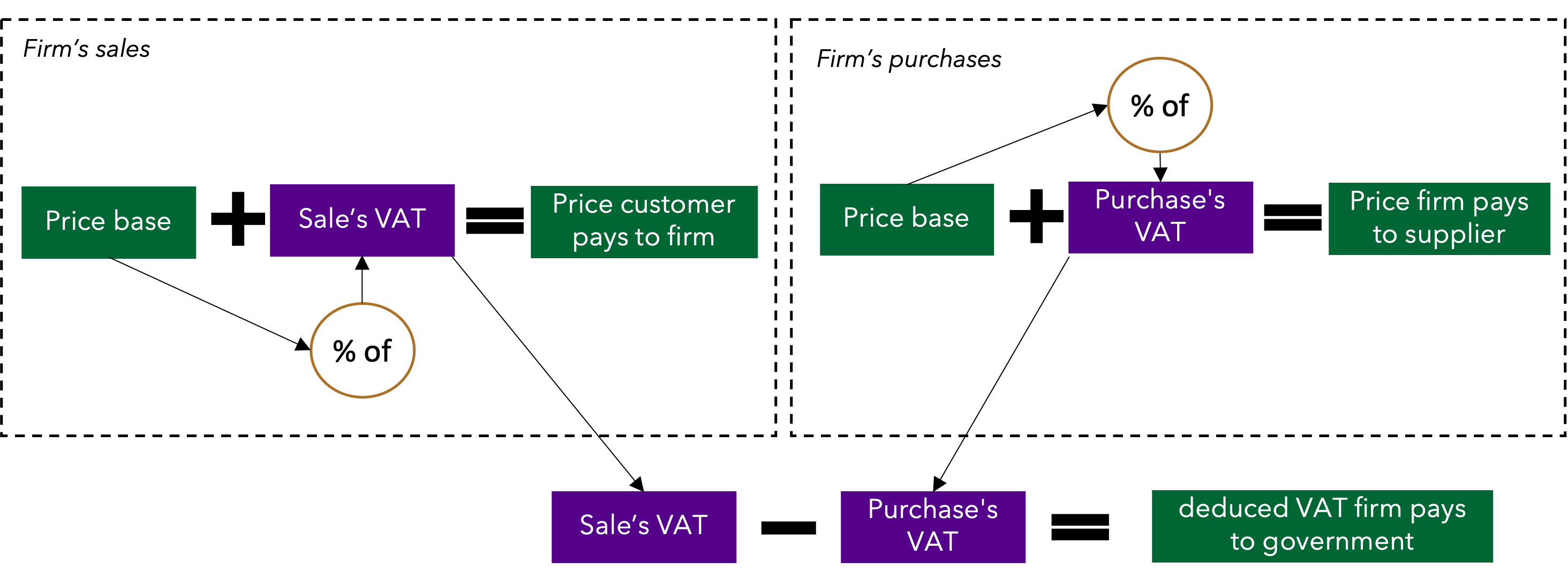

Another important tax that a business has to pay is Value Added Tax – VAT (Exhibit 8-17). This tax is calculated on any sale and is usually a fixed percentage. The principle of calculation and payment of this tax is slightly different from the profit tax. Value added tax is calculated by deducting VAT of sales by VAT of purchase. When making a sale, the organization issues a VAT invoice and adds a percentage determined by the state to the value of the product or service. The VAT amount is included in the invoice as a separate amount and added to the value of the goods or services. The buyer pays the seller the full amount including VAT. The seller is obliged to transfer the received VAT tax to the state once a month or quarterly, depending on the country. However, the seller, in order to carry out his activities, also makes purchases from his suppliers, which also include VAT on top of price into invoice. Thus, the seller can reduce the VAT tax payable to the state by the amount of VAT that is from the invoices received from the suppliers. The same period, one month or three months, is used for accounting, so at the end of the period, the so-called sales VAT is simply deducted by value of purchase VAT. This system is not complicated, but for entrepreneurs who are in a country that does not have such a tax, it may seem awkward and unusual. For example, in the USA, such a tax is not collected at the state level, and individual states apply a tax similar to VAT, which is called the goods and services tax. Thus, for US entrepreneurs, the VAT tax and the nuances of its deduction or even return may be hard to understand, especially if an organization has to trade with European countries, where the tax is one of the main sources of income for the state budget. VAT in Europe ranges from 16 to 21 percent. Exporting goods to another country is not subject to VAT, but some countries apply import VAT. Thus, when a buyer buys a product from another country, for the agreed price, in that case he pays a percentage of the value of the product, so called import VAT. After the subsequent sale of this product, the sales VAT paid to the state is reduced by the amount of import VAT. It is crucial to mention that only business enterprises that are VAT payers can make VAT deduction. End users, especially in the B2C – business to customer segment, are natural persons, so they are effectively the final payers of VAT, as they have no possibility of deduction or return. In certain cases, if the product is taken out of the country, for example in an airport store, such sale of the product can be considered as an export and there isn’t any requirement for the buyer to pay VAT.

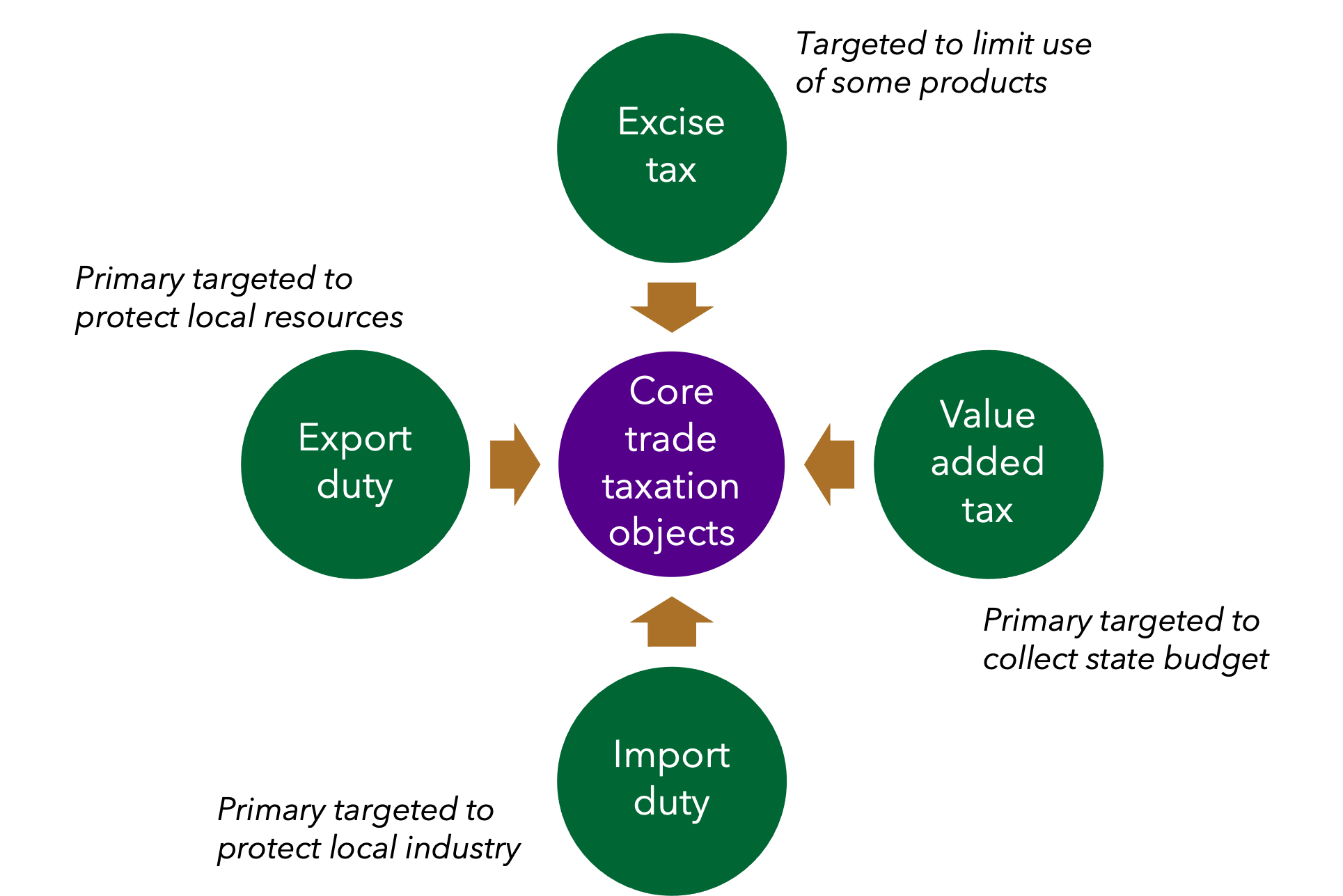

Another group of taxes is related to tariff restrictions on trade – that includes, import or export tariffs (Exhibit 8-18). Customs duties depend on the specific group of goods. Since the purpose of import tariff is to protect domestic producers from cheaper producers in other countries, it is very important to assess them in international business.

Ex. 8‑18 Taxes to consider for international business

Keywords: trade tax, import duty, excises, import VAT

It is possible that the import tariff will make the product uncompetitive in the market of the selected country, since the tariff will be included in the final price of the product to the consumer. Import tariff is very often charged together with import VAT when the goods are brought into the country. For some groups of goods, tariffs may exceed the price of the goods several times. This tax is extremely important for international business, when it is expanded through export. Due to customs, international companies sometimes decide to make foreign investments and produce goods in a country where it is not worthwhile to import already manufactured goods due to high tariffs.

Another tax that makes the product more expensive for the end user is an excise. An excise is applied to such goods, the use of which the state wants to reduce due to the damage it causes to the environment or human health. For example, cigarettes and other tobacco products, alcoholic beverages, gasoline, diesel is taxed with excise. Each country sets its product specific excise rate, which are usually calculated per unit. For instance, the excise is levied on a ton of gasoline, a litter of alcohol or a pack of cigarettes. Unlike import tariff, an excise applies equally on both imported and domestic goods, so the decision to open a factory in a foreign country instead of exporting does not change anything here. On the other hand, an excise applies equally to local producers, so it has little effect on competition with local businesses. Excise affects the market itself. When the product specific excise is raised, the consumption of such product usually decreases, so when planning to export in a specific country, it is important to evaluate not only the current market size but also monitor constantly whether the government is planning to reduce the market size by excise.

Although excise, when applied to fuel, is partly considered an environmental tax, some countries introduce additional environmental taxes, such as an air pollution tax or a CO2 tax.

Ex. 8‑19 Taxes to consider for international business

Keywords: tax objects, property tax

Since many countries in the world are concerned about the ongoing climate change, and one of the reasons is the increase in CO2 emissions by burning fossil fuels, the countries of the world agreed in 1997 by signing the Kyoto Protocol that they would take steps to limit the burning of oil products. It has been widely accepted within the industry that factories will pay a CO2 tax through the purchase of an emission permit. Each country received a certain quota of annual CO2 emissions, but if the country has no industry and emits no CO2 or emits less than the allocated quota, the country can sell the unused part of quota to another country. A country that has a lot of industry buys these emission permits from other countries that sell them. Thus, industrial companies pay for the right to emit CO2 emissions. The European Union, being the initiator of the Green Deal, plans to apply this principle in the transport sector as well, and in the third decade of the 21st century, a CO2 tax will probably be introduced for transport companies as well.

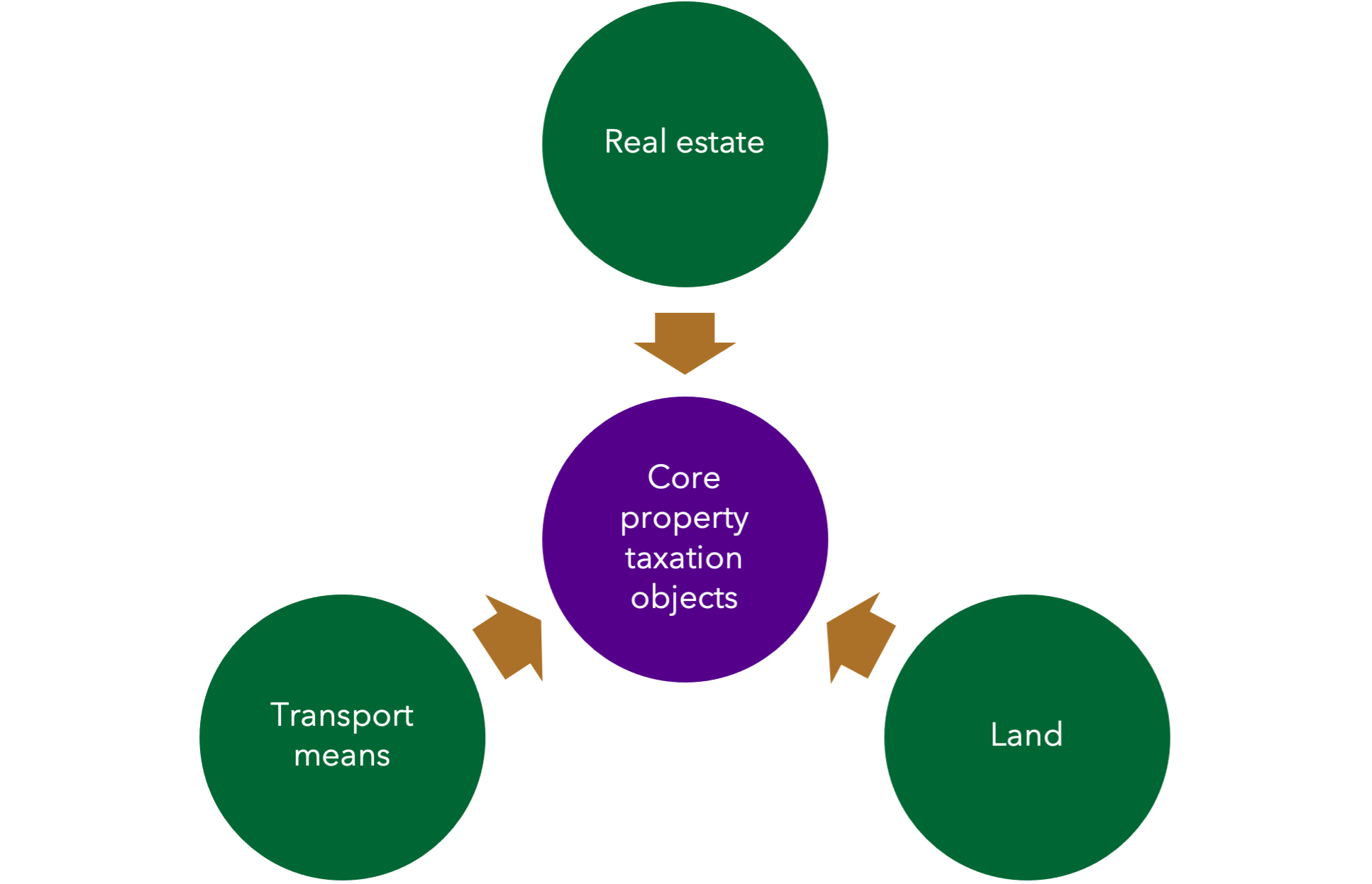

Property taxes play a significant role in international business too. In various countries, property taxes are imposed on different objects, usually real estate, land, in some countries – on cars or other equipment (Exhibit 8-19). Property tax is distinguished by its independence from the activity and income level. Property tax usually ranges up to 3 percent of the property’s value annually. Property tax compels property owners to use their property efficiently. Therefore, when considering investments in another country, it is crucial to evaluate the portion of income or profit that will be allocated towards property taxes. Many countries offer property tax incentives to attract investors particularly in free economic zones.

Share or comment this information on your social media:

Fundamentals of global business

First edition

For citation:

Jarzemskis A. (2025). Fundamentals of global business, Litibero publishing, 496 p.

Full scope of the book is available in various formats

C.8. Political, legal and economic environments in global business

About author

The author has been teaching at several universities since 2005. 40+ scientific publications, 10+ international research projects. More about author.